RPG Life: Thinking Slow, Compounding Fast

The appointment of Mr. Yugal Sikri at RPG Lifesciences felt like a random event in my journey, though a very positive one. My only effort had been to buy into RPG Lifesciences back in 2014, at a time when everyone else was chasing the US generics story (Lupin and Sun Pharma were the leaders back then). My first trade was in late 2014, and I gradually completed my allocation by early 2015.

The core of my investment thesis was simple: how can a company with RPG Group heritage and the Sarle India legacy remain a nano-cap forever? I was ready to wait, patiently, for years if needed. Then, unexpectedly, Mr. C.T. Renganathan was appointed MD in early 2015, just as I was finishing my allocation. Optimism and anticipation took over the market, and by mid-2016, RPG Lifesciences had become a multi-bagger, at a time when some of the big generic pharma players began showing cracks.

Yet, the operating margins remained stubbornly flat. I decided to take some profits, selling nearly 40% of my holding. My thinking was simple. I wanted to have my cake and eat it too. This was not about price appreciation, it was about the fundamentals. The stock was rising on optimism, but the business itself was not yet transforming. Had the fundamentals improved, I might have bought even more.

Between 2016 and 2018, the stock largely traded sideways, showing little improvement in the business’s economics. Then came the crash of 2018-2019. Even the appointment of Mr. Yugal Sikri in late 2018 could not stop the slide. I chose to sit tight and let him assess the situation. Having booked partial profits earlier, I was shielded from permanent capital erosion, but watching the stock fall was still unnerving. No one likes to see their holdings butchered!

The turning point came with the annual report of summer 2019. There was a clear, positive shift in tone and intent. I resumed buying. By the time I completed my “re-stocking” later that year, COVID was looming. Yet, the way Mr. Sikri navigated the crisis and the changes he introduced began to show results almost immediately. Sales growth outpaced the Indian Pharmaceuticals Market (IPM), margins, cash flow, and the balance sheet all improved. I was over the moon.

This note is both a reminiscence and a tribute to one of the finest managements India has produced. Mr. Sikri has not just driven life sciences excellence, but also delivered a masterclass in leadership, in connecting with all stakeholders, and in executing with clarity and vision.

How Yugal transformed RPG Lifesciences

Since taking charge in late 2018 (FY19), Yugal introduced a comprehensive Transformation Agenda at RPG Lifesciences. He guided the company through phases of “Fundamentals Fixation,” “Process Excellence,” and “Sustainable Profitable Growth,” setting the stage for its current Scale-up journey.

1. Process changes

Yugal shifted the focus from maintaining legacy systems to a Five Pillar Growth Strategy for Domestic Formulations and a targeted niche strategy for International business.

He introduced a Life Cycle Management (LCM) approach for legacy brands, launching 24–25 line extensions to open new indications and reach new customer segments.

For the first time in the company’s 50-year history, he launched a structural cost-reduction project, re-engineering 13 key SKUs that contributed over 80% of domestic turnover.

Yugal imposed strict discipline on sales hygiene, reducing market expiries from over 4% in FY19 to less than 1.5% in FY23.

Evidence & outcomes:

The Domestic Formulations business grew at 2.5 times the market rate (18.8% vs. 7.6% market growth) in FY24.

The legacy brand Naprosyn crossed INR 50 crore, reaching INR 74 crore in FY24, moving toward a “mega brand” target of INR 100 crore.

Sales force productivity improved from INR 3.4 lakh per person (FY19) to INR 5.8 lakh (FY24).

2. Culture changes

Yugal focused on building a high-performance culture, embedding innovation and employee well-being into the company’s DNA.

RPG became the only global group to make “Happiness” a theme. Yugal formed a Happiness Council, launched dedicated “Happiness Quarters,” and linked these initiatives to Managers’ KRAs.

Innovation moved from a buzzword to a system, with over 120–130 projects across departments, celebrated through internal “Innovation Festivals.”

Regular communication channels like Monthly Happiness Forums and the “Navigators” platform allowed ideas to flow directly from the sales team to leadership.

Evidence & outcomes:

Organisational happiness rose from 83% to 87% over three years.

The company received the Jamnalal Bajaj Award for Fair Business Practices and was named a Top 500 Value Creator by Dun & Bradstreet.

3. System changes

Yugal also drove structural realignments and digital transformations to modernize the company’s infrastructure.

Industry-first platforms like RPGserv reached over 90,000 doctors, while backend systems including e-QMS, e-DMS, and e-LMS optimised internal processes.

He streamlined roles, removed duplication, and optimised the span of control.

Investments of over INR 140 crore modernised API and formulation plants, meeting EU GMP and TGA Australia standards.

API operations were consolidated in Navi Mumbai, freeing and monetizing 15,015 square meters of land, generating INR 144.9 crore for future growth.

Evidence & outcomes:

EBITDA margins rose steadily from 10.4% (FY19) to 26.4% (FY25).

The company became debt-free, with a cash surplus of INR 266 crore by FY25.

ICRA upgraded the long-term rating from A to A+ (Stable).

“What’s noteworthy is for the fourth consecutive year, we have year-on-year upward trajectory on a number of financial parameters. Sales has grown consistently more than the market for the last four years. All profitability indices, EBITDA, PBT, PAT all have registered year-on-year consistent uptrend or superior growth. Both PBT and PAT has multiplied, has grown 6x in the last four years.

Similarly, margins have also registered consistently year-on-year growth. EBITDA has moved to 21% in FY ‘23. PBT is up from 4.4% in FY ‘19 to 17.9% now. PAT is up from 3.2% to 13.2% now. Similarly, cash flow has also registered one of the remarkable growths from minus INR14.5 crores in FY ‘19, I’m pleased to share with you we are INR115.2 crores this year.

And all of the above with a very strong iron grip on the hygiene. In fact, even on the hygiene front, we have almost reached the industry benchmark with the -- we were around 4%-plus expiries in FY ‘19, we are now down to less than 1.5%. Reaching here has been a journey indeed. If I recap FY ‘19, we had the first thing to do was getting into the business and fixing the fundamentals. From there, we move to process excellence and then to sustainable profitable growth.

And I’m happy to share with you today, RPG Life Sciences stands amongst the best in the competitor group of less than INR1,000 crores turnover with a number of our margins, a number of our financial ratios matching up or even number 1 compared to the peers in the less than INR1,000 crores or INR2,000 crores turnover company.

… I must share with you that our cost reduction story is structural. What we mean by structural is that the basic components of the cost, particularly the ones which are contributing greater proportion, have been addressed from the fundamental standpoint.” - Yugal Sikri, Earnings call, May 02, 2023

"FY24 marked the 5th year of our Transformation Journey of consistent, uninterrupted, upward trajectory of Sales, EBITDA, Margins, ROCE, ROE, EPS and Cashflows with our company emerging as a benchmark company amongst the comparator companies in a number of key financial metrics viz. Margin, Leverage, Return, Liquidity and Valuation ratios” - Annual Report, 2024

A masterclass in system 2 leadership

Yugal’s transformation of RPG Life was not just a business turnaround. It was a behavioural reset. By slowing the organisation down, questioning its instincts, and redesigning its decision environment, he proved that the most durable transformations begin not with strategy, but with how people think.

To understand RPG Life Sciences and Yugal’s leadership, I find it useful to look at his journey through the lens of Thinking, Fast and Slow and Nudge. Not because he set out to apply behavioural science, but because his actions instinctively followed its deepest principles. When Yugal joined RPG Life as MD, he questioned almost every process and interaction across the organisation. In doing so, he forced the company to pause, reflect, and think. What he really initiated was a shift from automatic, inherited behaviour to deliberate, conscious decision-making. In Kahneman’s language, the organisation moved from System 1 to System 2.

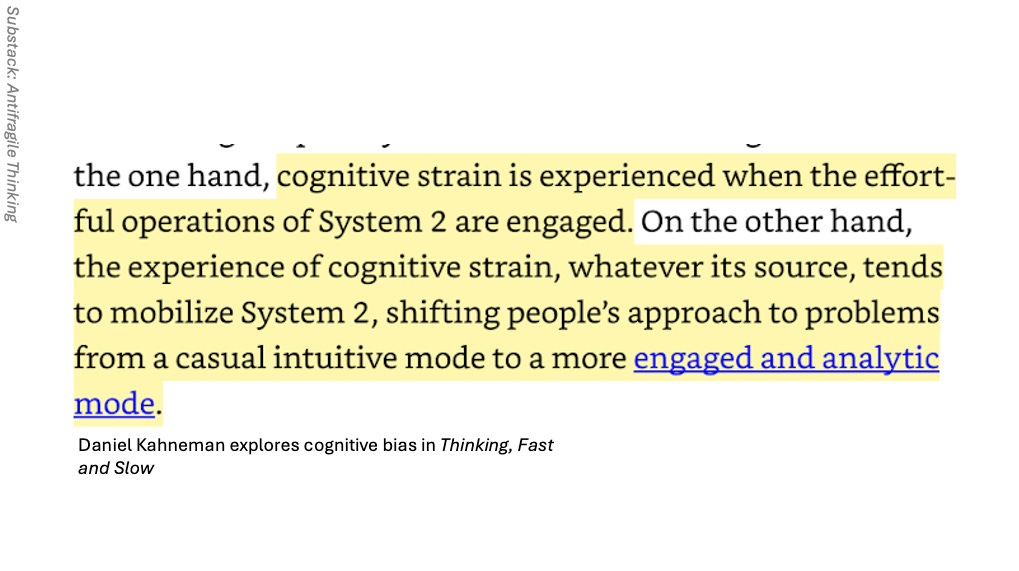

Before Yugal, much of the organisation was running on autopilot. Processes existed because they always had. Decisions were made quickly, intuitively, and often without questioning first principles. By asking hard questions and refusing to accept standard answers, Sikri introduced cognitive strain into the system. Kahneman tells us that cognitive strain activates System 2, the slower, more analytical mode of thinking. That is exactly what happened. Teams could no longer rely on familiar templates or legacy logic. They had to engage, analyse, and justify. What looked like disruption was actually discipline. What felt uncomfortable was the organisation learning to think again.

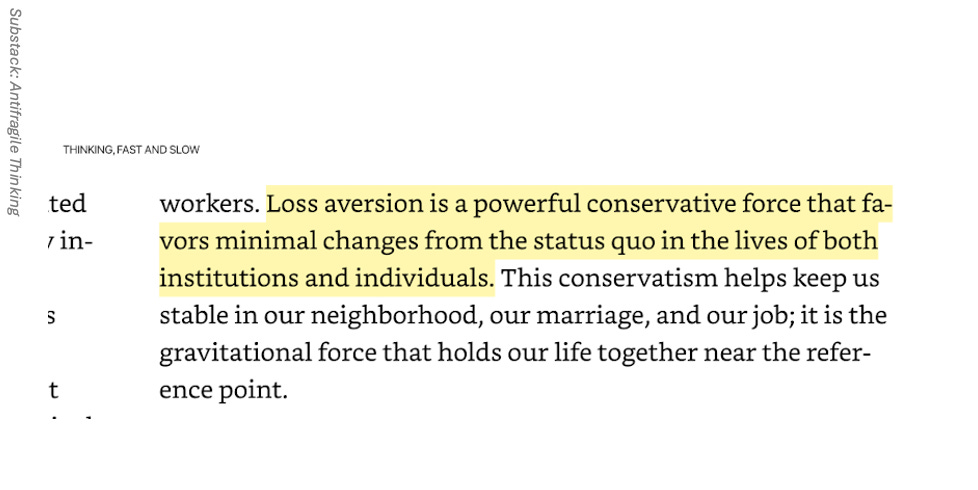

The structured transformation agenda was also a direct assault on status quo bias. Organisations, like people, prefer to stay where they are, even when change is clearly needed. Inertia is powerful, and most people quietly default to “this is how we do things here.” Yugal broke that inertia by creating a clear, phased journey. Fundamentals first. Then process excellence. Then sustainable, benchmarked performance. By laying out this path, he changed the default setting of the organisation. People did not have to guess what mattered anymore. The new direction became the path of least resistance, which is exactly how lasting change takes root.

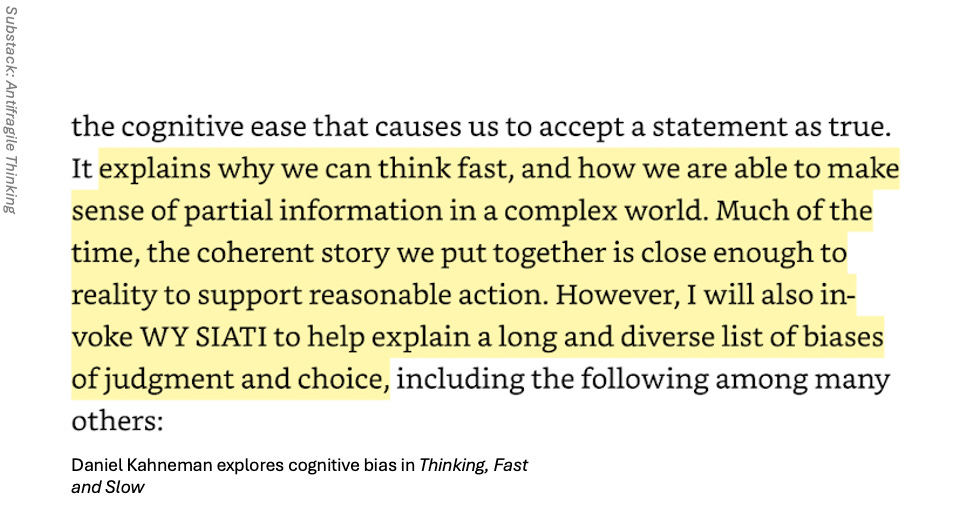

Another quiet but critical impact of this approach was how it countered what Kahneman calls WYSIATI, what you see is all there is. Organisations often build convincing success stories based on partial information, ignoring hidden inefficiencies and unseen risks. By insisting on process excellence and by questioning interactions across the value chain, Yugal brought those blind spots into the open. Unknown unknowns were surfaced. Comfortable narratives were challenged. This reduced overconfidence and replaced it with humility, data, and a more complete view of reality.

One of the most underrated aspects of Yugal’s leadership has been his discipline in communication. The practice of updating shareholders every six months is not just good governance. It is a powerful behavioural tool. Hindsight bias makes us believe outcomes were obvious all along, especially when things go well. Regular, contemporaneous updates create a living record of intent, assumptions, and execution. They anchor judgment to the quality of decisions made at the time, not just the eventual outcome. They remind us that the six-year upward journey was not inevitable, but earned through consistency and course correction.

Perhaps the most profound application of behavioural thinking lies in how Yugal shaped culture. By introducing a happiness framework, embedding it into managers’ KRAs, and supporting it with digital platforms, he acted as a true choice architect. Rather than relying on speeches or slogans, he redesigned the environment in which people made daily decisions. Feedback became visible. Behaviour became measurable. Well-being stopped being an abstract idea and became part of performance. This is classic nudge theory. Expect human error, design for it, and gently guide behaviour in the right direction.

Seen through this lens, Yugal’s leadership was not about speed or heroics. It was about slowing the organisation down just enough to think clearly, choose deliberately, and act consistently. The transformation of RPG Life Sciences was not only a business turnaround. It was a behavioural reset. A shift in how decisions were made, how defaults were set, and how people were nudged toward better outcomes. In the end, the real scale-up did not begin with numbers or assets. It began in the mind.

Investor Lens

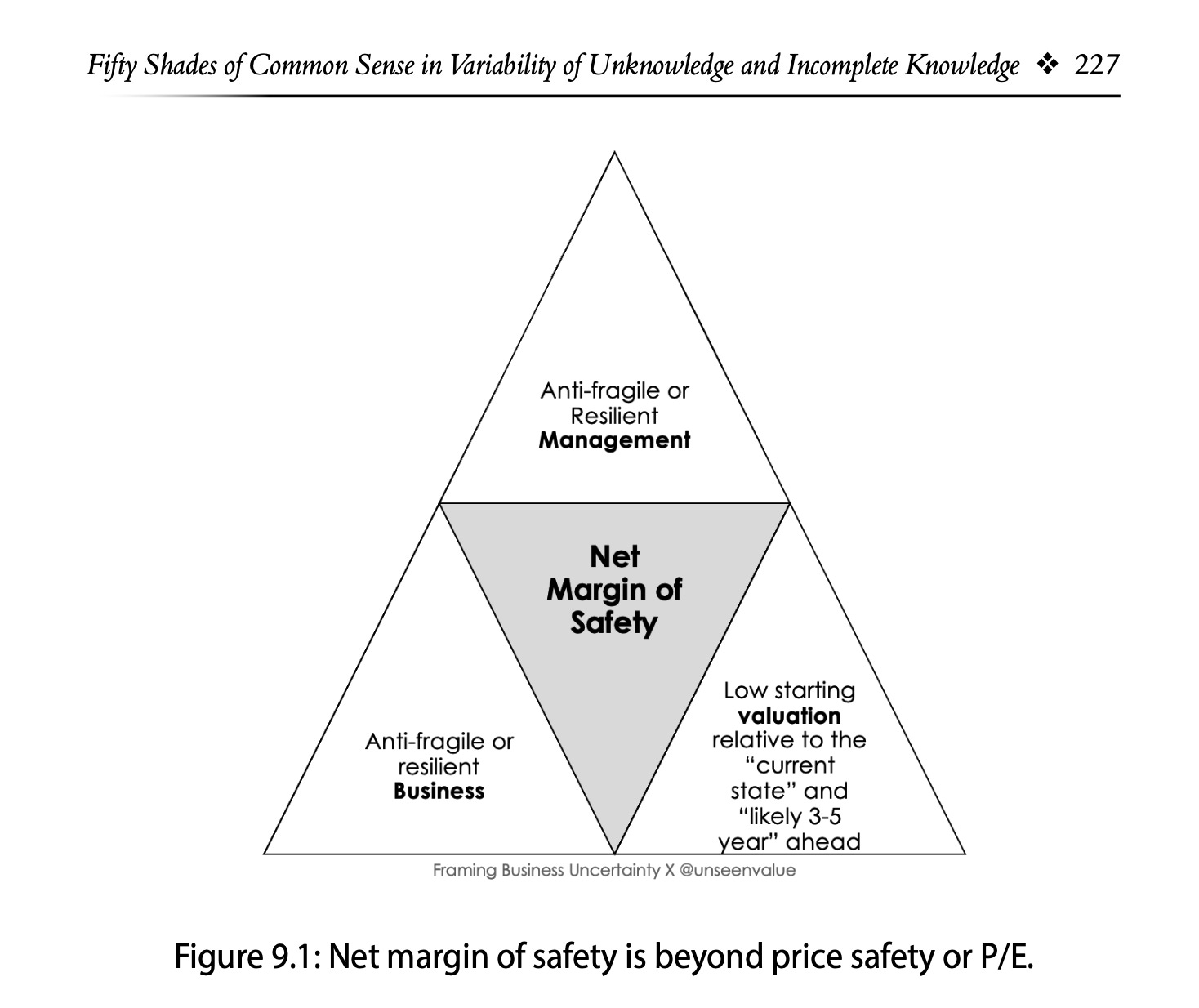

In my philosophy of value investing, leadership is not a soft variable. It is an automatic margin of safety. People run businesses, and over time they make thousands of decisions, most of them small, many of them invisible. Those decisions either compound value quietly or destroy it just as quietly. While price-to-value is the traditional way investors define a margin of safety, I believe superior leadership provides a living, breathing hedge against uncertainty. Good management absorbs mistakes, adapts to change, and navigates ambiguity in ways no spreadsheet ever can.

Source: Framing Business Uncertainty

One of the clearest differences between good and bad management is the kind of surprises they deliver. Weak leadership tends to disappoint. Strong leadership does the opposite. Great teams consistently deliver positive surprises, finding ways to exceed what investors originally expected. In a growing business, this matters enormously. When leadership keeps upgrading the business itself, intrinsic value rises after you’ve already invested. The margin of safety doesn’t just protect you, it quietly grows.

Leadership also shows up most clearly in how capital is allocated. Every rupee of free cash flow is a choice. Whether that money is reinvested in the business, used for acquisitions, returned to shareholders, or simply preserved, the quality of that decision determines long-term outcomes. In the hands of capable leaders, capital compounds. Even if the entry price was not a screaming bargain, intelligent reinvestment over time can cover up a lot of sins. This is how good management protects investors from value traps. Value keeps growing while the market catches up.

Another under-appreciated source of safety is what Thomas Russo calls the capacity to suffer. The best leaders are willing to endure short-term pain in pursuit of long-term value. They invest when it hurts. They defend the moat even when profits dip and criticism rises. This discipline is hard, and it is rare. But it is precisely what preserves competitive advantage and ensures the business is stronger five or ten years down the line than it is today.

Leadership becomes most visible when things go wrong. In moments of extreme stress, when markets crash and fear takes over, price tells you nothing about business quality. What matters then is whether the company survives and emerges intact. Proven leadership, conservative balance sheets, and calm execution ensure the business is not snuffed out at the bottom. In fact, the best teams often use crises to strengthen their position while competitors retreat.

At the foundation of all of this lies trust. The biggest risk an investor faces is not volatility, but misaligned or dishonest leadership. When management wastes, diverts, or abuses cash flows, no valuation can save you. Aligning with leaders who are honest, rational, and shareholder-oriented removes entire categories of risk, from accounting landmines to ego-driven acquisitions. As the saying goes, there is no way to make a good deal with a bad person.

For me, this is why leadership matters so deeply in investing. Great management does not eliminate risk, but it reshapes it. It turns uncertainty from an enemy into an ally. And over time, it becomes the most reliable margin of safety of all.

This is a tribute to the remarkable Mr. Yugal Sikri.

Should I re-enter RPG now or wait?

In the case of RPG Life Sciences, the market’s valuation has always been closely tied to the quality and visibility of execution. When execution was strong, consistent, and clearly evident in the numbers, as demonstrated during Yugal’s tenure, the market was willing to value the company at close to 4x sales. That valuation was not driven by hope or narrative, but by measurable outcomes such as sustained sales growth well above the Indian Pharmaceutical Market (IPM), improving margins, and disciplined capital allocation.

Source: Screener.in

In recent quarters, following Yugal’s departure, this equation has begun to change. Sales growth, which had consistently outpaced the IPM, has slowed sharply. This deceleration has naturally raised questions about the effectiveness and efficiency of the new leadership team, particularly around execution intensity and strategic clarity. When execution weakens or becomes less visible, the market’s willingness to pay a premium multiple also diminishes.

Source: Screener.in

It is important to recognise that the earlier 4x sales valuation was earned on the back of solid, visible, and repeatable execution. In the absence of that same level of confidence today, the market will apply a higher margin of safety. As a result, the valuation multiple that once held at 4x sales cannot be assumed to hold under current conditions. Until execution once again becomes clear and compelling, a similar value zone for the stock is likely to sit below 4x sales, reflecting the increased uncertainty and execution risk perceived by the market.